RBI’s move to settle loans of wilful defaulters will a have serious impact on the banking system. It is the middle class people whose deposits will be used for writing off loans with a small recovery.

By Shri Thomas Franco, Ex- General Secretary, All India Bank Officers’ Confederation (AIBOC) and Steering Committee member at the Global Labour University

Reproduced from Centre for Financial Accountability, www.cenfa.org

Wilful defaulters and companies involved in fraud can go for a compromise settlement or technical write offs by banks and non-banking finance companies, as per the new RBI circular.

“A wilful defaulter is a borrower who refuses to repay loans despite having the capacity to pay up,” as per the definition. And, “a fraudster is one who intentionally cheats the bank with false documents/information and misappropriates the money.” Both are criminal offences.

Till 2019, the RBI had clearly instructed the banks vide its circular notification ‘RBI/2018-19/203, DBR No.BP.BC 45/21.04.048/2018-19 dated 7.6.2019 vide para 34’ as “borrowers who have committed frauds/malfeasance/wilful default will remain ineligible for restructuring”.

This was a reiteration of the earlier instructions which existed for long and were in force till June 8, 2023. Shockingly, the central bank modified its circular ‘RBI/2023-24/40 DOR.STR.REC.20/21.04.048/2023-24’, dated June 8, 2023, allegedly to help wilful defaulters and fraudsters who are criminals. It says in para 6(ii), “Proposals for compromise settlements in respect of debtors classified as fraud or wilful defaulter, as permitted in terms of clause 13 of this annex, shall require approval of the Board in all cases.”

Para 13 (Annex) Regulated Entities may undertake compromise settlements or technical write-offs in respect of accounts categorised as wilful defaulters or fraud without prejudice to the criminal proceedings underway against such debtors.

Since 2014, the Government of India has not appointed officer directors and employee directors in public-owned banks and the Boards have political supporters of the ruling party. The RBI has not questioned the non-appointment of the officer and employee directors.

One of the deputy governors of the RBI recently lamented about the functioning of the boards while addressing the board of directors of public-owned banks.

So it’s anybody’s guess how boards will approve compromise settlements. They don’t have any accountability unlike the officers and employees. Without the watchdogs from associations and unions, the Boards have become opaque and their decisions are not even available under the Right to Information.

We also know what happens to the cases once compromise settlement is arrived at.

This is going to have a serious impact on the banking system. It is the depositors from the middle class whose deposits will be used for writing off loans with a small recovery. And, the criminals can once again avail loan! His CIBIL rating will improve as his data will be cleansed. Naturally, the good borrowers who are promptly repaying will start defaulting. This will affect the banks. Except the borrowers who have given strong collateral, others will tend to default and expect write off.

Who are the people who are going to be benefitted? In 2018, it was reported that out of 5,600 wilful defaulters, 15% were from Gujarat.

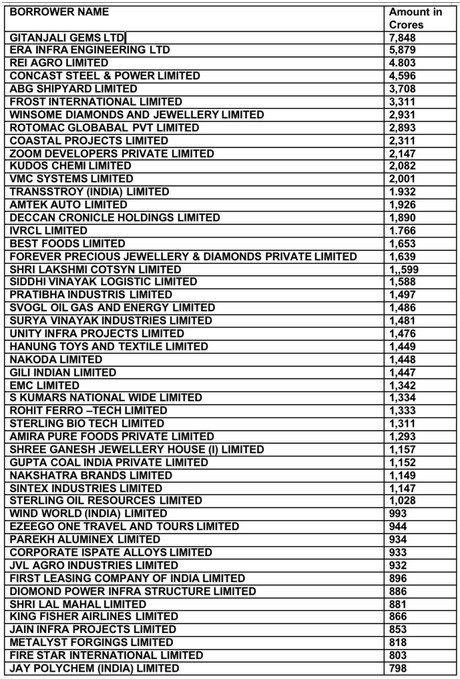

Here is the RBI data on top 50 wilful defaulters in 2022:

ABG Shipyard (Rishi Agarwal), Winsome diamonds (Jatin Mehta), and many of the other wilful defaulters are close to the corridors of power. Some are already abroad. ABG Shipyard’s Agarwal, who cheated 28 banks to the tune of Rs 23,000 crore, can now have a compromise settlement.

Similarly, Mehta, who is a close relative of Adani, who ran away, can now return. The same could be the case with Vijay Mallya, Mehul Choksi, Nirav Modi, and others. They will fund the election campaigns.

The National Company Law Tribunal (NCLT) is already helping the defaulters. Even the Parliament Standing Committee has strongly criticised NCLT. In the last 10 years, NPA reduction due to write off stands at Rs 13,22,309 crore.

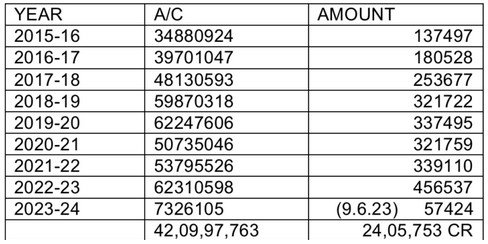

There is going to be another bigger political gain. In the last nine years, the banks have given Mudra Loans worth Rs 24,05,753 crore to over 42 crore borrowers up to June 9, 2023. See the year-wise sanctions given below:

The finance minister has been giving targets to the government-owned banks which are also forced to lend to non-banking finance companies for on-lending and co-lending. In many places, the ruling party cadres tell the borrowers that this is a gift and not to be repaid. So, NPAs are increasing and banks are writing off 25% and claiming 75% from the Credit Guarantee Fund. But the borrower’s CIBIL score gets affected. Most of them are wilful defaulters. Now they can pay a little, clear the CIBIL score, and borrow again.

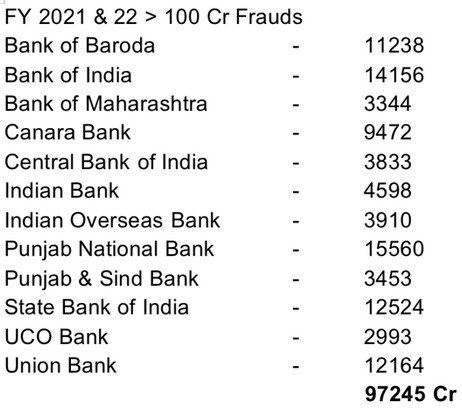

Let’s take a look at the frauds. In 2023 alone, 13,530 frauds were reported by banks to the RBI. In 2021 and 2022, public-owned banks reported Rs 97,245 crore frauds in accounts outstanding above Rs 100 crore alone. See the bank-wise list below:

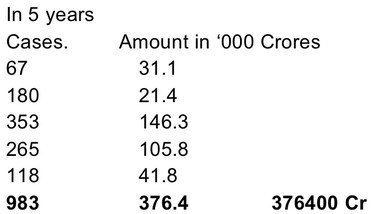

In the last five years, banks have reported 983 frauds above Rs 100 crore to the tune of Rs 3,76,400 crore. Is it correct to compromise with these criminals? This is a clear loot!

Through the NCLT, established under the Insolvency and Bankruptcy Code, lakhs of crores of public money has been written off in the name of haircut. Banks are given some capital to carry out this siphoning off of money to few rich corporates. They in turn support the political party through electoral bonds and other ways.

The write offs of smaller loans provides dividend in the elections as the number is huge.

The bank’s balance sheets are shown as clean with high profits at the cost of depositors who get less interest, pay more bank charges and small borrowers who pay high interest. Now it will be easy to sell them in the name of privatisation!

The RBI is being used as a tool for political gain, which is a violation of law.

Section 21 of the Banking Regulation Act reads: “[The] power of Reserve Bank to control advances by banking companies (1) where the Reserve Bank is satisfied that it is necessary or expedient in public interest or in the interests of depositors or banking policy so to do, it may determine the policy in relation to advances to be followed by banking companies generally.”

This compromise settlement of wilful defaulters’ loans and fraudsters loans is neither in public interest nor in the interest of depositors. It is a violation of law. This has to be withdrawn.

All India Bank Officers Confederation and All India Bank Employees Association have strongly condemned the RBI and demanded withdrawal of the instructions failing which the depositors will be affected and defaults will increase and there will be no faith in the system. This may lead to a collapse.

Political parties and the public will have to rise to the occasion. Banks can’t be used for political gains at the cost of more than 100 crore small depositors.